Stocks A to Z / Stocks B / Berkshire Hathaway (BRK.A)

No. of Recommendations: 36

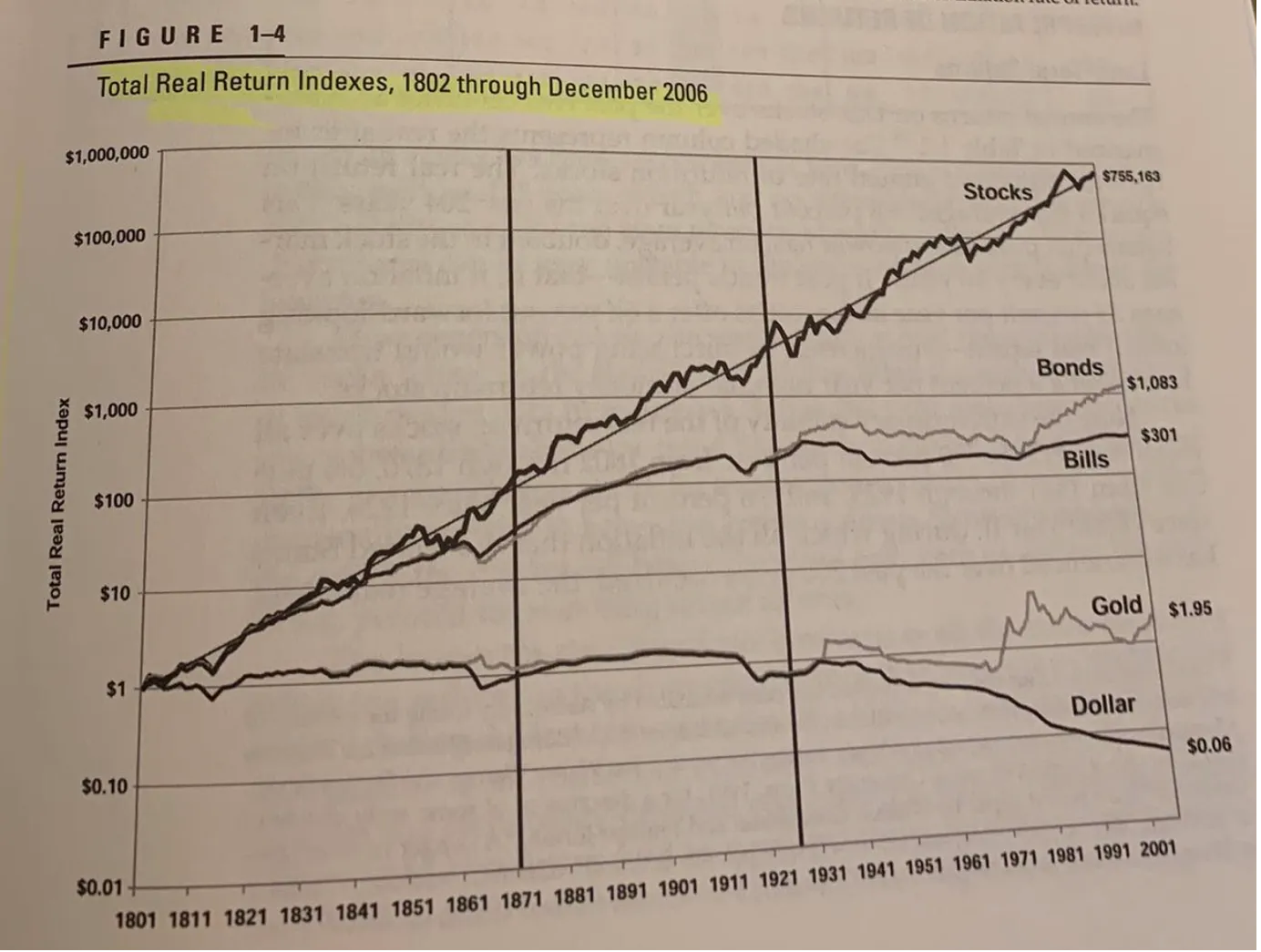

My favorite data set presented by Jeremy Siegel is the comparison of the real total returns* of stocks, bonds, cash and gold - we know the relative long-term returns, but it is good to have a reminder occasionally, and to see how dramatic the contrast is.

https://substackcdn.com/image/fetch/w_1456,c_limit...As many others have observed, the really tough time for investors was during the 1970s, where you had about a one and a half decade stretch without any real total returns. Investing from the peak in 1929 would have led you to wait pleasantly less time - closer to only one decade - before you were permanently in the positive, owing to the deflationary situation and spending power not falling so much. As testing as it would be, I expect I could handle one decade (after all, that is similar many starting in March 2000 and having to wait through 2009, and longer, before the region of permanent positive returns had started).

- Manlobbi

* This is the return that matters to you - it is your actual increase in spending power owing to your investing enterprise. Ignoring dividends is crazy, given that they constitute the bulk of your return historically (in recent year the trend is towards re-investing cash and keeping the dividend payout ratio very low (relative to the past), and applying buy-backs, partly as these are

both more tax friendly, and partly because this is just the fashion for now). Accounting for inflation turns it from a number game into a real life game.

No. of Recommendations: 29

Siegel's 2023 edition of Stocks for the Long Run has a more up-to-date version of the above linked chart. The date range to 2021 (extra 20 years by comparison)

Here's a link to the chart:

https://photos.app.goo.gl/5ESJPGicC8BgiCVq9

No. of Recommendations: 1

Thanks both, stocks beating the other asset classes and beating 'em by far and over a long period couldn't have been summarised better than the graphs you shared. A picture is worth a thousand words afterall. Wish there could be a comparison with the real estate returns over a long period too though it would be a challenge to find a good marker for that.

No. of Recommendations: 27

Wish there could be a comparison with the real estate returns over a long period too though it would be a challenge to find a good marker for that.

Real estate is a productive asset, but the returns are worse than what you would get from taking the rental yield and assuming capital gains a percent above inflation. If one assumes rental yields averaging 4% that we have a real long term return of about 5% per year. At first this appears not far below the real returns from common stock of 7% or so.

The trouble, sometimes not cited enough, or admitted by the property investor, is the effect of repairs and upgrades. In practice to maintain just the going rental yields, the bathrooms and kitchen are renovated once every 20 years or so. Or you let the cracks builds and style go out of date and the rental yield sinks.

All in all the costs consume around 2% of the property value annually as a heuristic (the costs are a little inconspicuous as it doesn�t hit every year but you can have a good run and then have to do a massive re-work or even demolition after 50 years or so, or the property re-priced to assume such cost ahead).

So now you are down to real returns of about 3% after subtracting the 2% depreciation charge (renovations and repairs).

Council bills and other taxation (not capital gains) costs in excess of the near zero running costs on stocks.. I won�t account for this bur you really have to subtract a little more again for this.

You can try to increase this 3% return with leverage (use of a mortage), but historically this isn�t as good as it seems because the (rental yield after costs), plus (nominal capital gains), need to be higher than the (lending rate) in order for the leveraging to actual provide a benefit. Mortgages are now take because either the buyer cannot afford the quote, or they don�t want to pay the quote because they have better uses for the capital (such as stock investing).

Even as recently as the 1950s, homes were viewed as a place to live and if you told someone you were buying a house to try to resell it at a higher price, the response would be: �Well, I'll be hornswoggled! Are ya crazy? That's a wild-eyed guess if I ever heard one, and I reckon you're bold as brass for slingin' it out there! But, dagnabbit, I ain't got a hankerin' it'll pan out for ya, partner.�

Times have changed, with the massive increase in availability of leveraging making homes far more expensive. The change to then and now has lowered the rental yields, so capital gains will be necessarily lower than the past - and likely about inflation, with real returns after costs and taxes only a percent or two above inflation.

On the other hand, many like to renovate their own house (or build) which produces value, and possibly passion, so there are always abundance nuances - but the baseline investment comparison with stocks is far less competitive than it can at first appear when just adding rent income and capital gains, and comparing that to stock index total returns.

- Manlobbi

No. of Recommendations: 6

so true. Any real return I have made in RE has been getting lucky catching episodic inflation over a short period in select highly desired markets.

No. of Recommendations: 21

Amen to what Manlobbi and Longtimebrk wrote. Our commercial real estate properties have been our lowest return and highest personal involvement investments. Put another way, the properties we bought after the GFC represent a considerable opportunity cost compared to what our same era parallel investments in equities have produced. It�s a circle of competence thing coupled with the capricious nature of the folks renting properties.

In an ironic way the properties have given insights into to some equity investment areas:

Waste management and Dollar Stores. When there are eight (8) medium sized commercial haul away construction dumpsters of stuff taken out of one (1) house, you get insights into how the Dopamine effects drive folks to repeatedly buy crap stuff. In this clean-up journey we also witnessed the role of landfill space. Siting and approving new landfills is quite difficult. If Waste Management or Republic Services ever have a market swoon to a Buffett type PE, I will be loading up the truck. There are hundreds of thousands homes with crap that someone will one day be hauling to a landfill. Landfill dumping fees continue to rise because of all the above factors.

Uwharrie

No. of Recommendations: 10

�the properties we bought after the GFC represent a considerable opportunity cost compared to what our same era parallel investments in equities have produced. It�s a circle of competence thing coupled with the capricious nature of the folks renting properties.�

Interesting & makes sense. Reminds me if a lesson my Dad (and I) learned. In the 1980s, along with a few buddies, he bought a new condo unit on the beach in Myrtle Beach and rented it out via mgt company for ~5 years before selling. After the HOA, mgt fees, storm damage, wear & tear, replacement of items, taxes, etc. he said it made no sense to hold on to it as an investment. Fortunately, he understood value investing & compounding and patience, but had to check the beach condo box. Good memories of the Grand Strand but it taught me a lesson wrt vacation properties & 2nd homes- I�ll pass and try to stay in my small circle of competence.

I find primary residence is pricy enough as it is. Btw, I thought in 2017 we�d perhaps make and extra payment here and there to perhaps pay off the 30 year mortgage (3.75%) early, but glad we have not, given the performance of Berkshire & equity markets.

No. of Recommendations: 8

Any real return I have made in RE has been getting lucky catching episodic inflation over a short period in select highly desired markets.

I think the key is the 'highly desired market".

I live in a former logging town gone resort boom town. In the last 15 years the median price has gone from 200k to 800k, but the riverfront properties have doubled that gain, from 500k to 4 million. I'm surrounded by real estate multi-millionaires. When I point out that BRK has gone from 100k to 800k in the same time, they correctly point out that their investment also gave them a place to live and RE is the easiest of all investments to apply a bit of debt related leverage. I hope they recognize they were lucky, and that RE is not often that lucrative. When we talk about retirement, they lean toward RE investments, and are skeptical of stocks. It is hard to blame them.

No. of Recommendations: 0

What town?

No. of Recommendations: 8

Even as recently as the 1950s, homes were viewed as a place to live and if you told someone you were buying a house to try to resell it at a higher price, the response would be: �Well, I'll be hornswoggled! Are ya crazy?

... Times have changed, with the massive increase in availability of leveraging making homes far more expensive.

The geographical differences can be extreme. At least from 1990 to 2015 house prices in Germany essentially were flat (neighbours, having bought a nice appartment in a typical city and area in 1990 sold it 1999 for exactly the same price). Even in the following years German house prices only partly caught up what was "missing" during all those years.

On the other hand in 2003 we bought the cheapest house in a nice modern suburb in New Zealand, living there for 2-3 months each year. 2008 we sold it for exactly double the price, so 100% gain. The prices continued to skyrocket and in 2018 that house again had doubled. That continued until Covid came.

New Zealand was one big casino, buying, selling, people talking about buying another rental property etc. Each year I predicted a housing crash, each year's "The Economist" global house price index showed NZ house prices among the most overvalued ones in the world (Ratio of house price to yearly household income) --- but that mattered to Kiwis not one bit.

So for at least around 20 years the housing market in New Zealand was the exact opposite of the German one. For Germans a private property was a losing (as investment) game, for Kiwis the best investment in their life, as good or better than stocks.

As I am on NZ please let me use the opportunity for an old Kiwi joke ("Atheist" board participants: Please do not read on):

A priest visited the most famous churches in the world. In Australia he went in a church in Sydney. He saw a red telephone with a sign: '$1 per minute'. Asking the local priest what it is about he was told: 'That's our direct line to God. It's so cheap because Australia is very close to God's own domain'. In Melbourne in a church, and in Adelaide, he always saw the same red telephone with the same sign: '$1 per minute'.

Then, in New Zealand, he went into a church in Christchurch. The same red telephone, but no sign with a price. Asking the local priest 'How much is a call to God?' he was told 'Oh, that's free. It's a local call'.

No. of Recommendations: 3

Bend, Oregon. I've watched it go from 20,000 to 110,000. The town still makes a disturbing number of "best of" lists. A common bumper sicker is "Bend sucks, don't move here". That said, we drove 20 minutes to ski a few runs yesterday, came back and had lunch outside on the deck, and watched beavers crawl up onto the lawn at dinnertime. I went mountain biking, paddling, and fly fishing right from my house this week, which is walking distance of a trendy downtown. There is a huge amount of investment and building going on, and I have to wonder if it is being over-built, but it is still relatively small compared to the bigger cities, so a little influx makes a big impact.

No. of Recommendations: 9

There are hundreds of thousands homes with crap that someone will one day be hauling to a landfill.

I volunteer for a disaster response organization and have responded to multiple hurricanes, floods and tornados. It is sobering to help haul all of someone's household goods to the street so the "FEMA truck" can collect it and haul it away. Some of it was junk, but some of it was cherished and priceless keepsakes. After my first deployment I called my spouse to say "we gotta get rid of stuff". I've been on that kick ever since. Too many in this country have insufficient insurance and can never be made whole after a disaster. I was never a fan of real estate as an investment but after these deployments my belief has only strengthened.

Rgds,

HH/Sean

No. of Recommendations: 4

In the last 15 years the median price has gone from 200k to 800k, but the riverfront properties have doubled that gain, from 500k to 4 million. I'm surrounded by real estate multi-millionaires. When I point out that BRK has gone from 100k to 800k in the same time, they correctly point out that their investment also gave them a place to live

While this is true, one still has to account for the 15 years of property taxes, they were $7500 (1.5%) at first, but rose to $60,000 (1.5%) by the end of their ownership (this is in fact most likely the reason they are selling ... because the annual expenses of owning that property have become too high). And they have been paying HO insurance for 15 years, it was inexpensive at first, but now with rising insurance rates and being riverfront, it's nearly $15k a year. And they put a new roof on in 2021 that cost $45,000. And the two new A/C units in 2022 were $14,000. The two hot water heaters in 2020 were $3k. The kitchen remodel in 2014 was $80k, and the master bath renovation in 2018 was $30k, and the small bathroom upstairs in 2019 was $20k, and the powder room just last year was $12k. The lawn guy charges $100/mo, so another $1200 a year, the pest control guy charges $40/mo. Gutter cleaning 2x year is $400, pressure cleaning all the surfaces is another $450 a year. And all sorts of other maintenance items. The price of the property went from $500k to $4M, but they didn't really live there "for free".

and RE is the easiest of all investments to apply a bit of debt related leverage.

This is true, especially in the USA with subsidized mortgages with extremely easy terms.

I hope they recognize they were lucky, and that RE is not often that lucrative.

Yep, luck plays a big role, like they say in real estate ... location, location, location.

No. of Recommendations: 4

one still has to account for the 15 years of property taxes, they were $7500 (1.5%) at first, but rose to $60,000 (1.5%) by the end of their ownership

A good list of the reality of home ownership expenses. I keep telling my friends who own several for rental income that there are easier ways to invest (even though I have made more in real estate than stocks).

You missed the tax bill by a mile. A house nearby just sold for 4.1 million. Taxes 15 years ago were $4000, and have gone up to $10,000. One of the advantage of a town full of fancy golf course second homes is that there is a big tax base, with fewer than average kids in residence to educate.

No. of Recommendations: 19

I see a high percentage of RE investors - usually folks who buy a house or three, or a duplex or such, for long term rental purposes, who are living in fantasy land and sort of hand waive taxes, repair bills, delinquent tenants, and the amount of time to devote to all of these. Let alone the frictional costs of buying and selling properties because of the entry feel to be on the MLS.

It can work out pretty well. In the early 70s dad bought a couple of duplex units, and made a few bucks with those. He bought two 4-unit apartments in the 80s and did a little better. He sold out when he retired in the late 90s. But boy did he ever spend a lot of weekends at them, painting and fixing and such. As did I - free labor!

If folks want RE exposure with about 1% of the time sink as actually owning and being a landlord, just go buy a REIT.

No. of Recommendations: 3

If Waste Management or Republic Services ever have a market swoon to a Buffett type PE, I will be loading up the truck.

I just moved out of the SF East Bay (to Lisbon), and was distressed to find that, after literally years of Waste Management telling me to schedule my two allowed bulky item pickups per year, they do not actually *do* bulky item pickups in that city. But it is fairly consistent with my overall experience of WM.

Oh well. Perhaps the city will fine me for last-minute junk left on the curb. If they can find me :-)

No. of Recommendations: 2

Real estate is a productive asset, but the returns are worse than what you would get from taking the rental yield and assuming capital gains a percent above inflation. If one assumes rental yields averaging 4% that we have a real long term return of about 5% per year. At first this appears not far below the real returns from common stock of 7% or so.

We have done very well with real estate, but make no mistake, there is nothing passive about it as an investment. IMO the key to doing well in real estate is being a small investor who can take advantage of the inefficiencies of the market, with many mistakes made by the listing agent who underprices the home for a quick sale. (More than once I have sold a property for 20%+ higher than the agents I interviewed felt I should START the listing at, with anticipation for decreasing the listing price.) Other than for cookie cutter homes, which we avoid, pricing a home takes effort and training that most agents just don't have. Or I guess you can be one of the real estate investor vultures that prey on mostly the elderly by reaching out to them to take the in need of improvement house off their hands, for a fraction of their current value, "without any real estate commissions", but that has never been our approach. Instead we look(ed) for homes in areas that have barriers to competition and new builds, multiple industries for employment, and dazzle factors that eliminate price only based rentals and encourage tenants to fight over the privilege to pay over market rents to live there. This allows us to require higher than typical credit scores for our market, which gives more protection for our investment, as they have something they value to lose in default.

I use the past tense, as I have concerns about investing in real estate these days, beyond no longer wanting to do the work required, though I will always consider my fall back positions in any personal residence I buy. (These concerns would apply to investments in REITS as well.) One is not always presented with a sellers market when needing to leave and area, so we like to reserve the right to hold on to it with it paying for itself. Some of the problems going forward include:

1. Climate changes: While area selection is still an option, I have no control over what seems to be an increasingly extreme climate that can put your property at risk and increase maintenance costs. Note that I automatically budget 10% of rents towards maintenance in my 10 year profit projection spreadsheet. While it could be a separate category, the climate changes have triggered insurance increases, even for areas that have not been subject to extreme conditions, which describes our area. Insurance doubled in 2023, up another 40% in 2024. One cannot account for these kinds of unexpected expense increases in a spreadsheet projection.

2. Property taxes: Similar to insurance, with the escalating prices of real estate, our taxes have skyrocketed. One year was over 30% increase, with all but one year in the double digits! This will vary based on location, but our area insists on re-assessing your property each year to reflect current value. No doubt, they will be slow to reduce that expense should the value go down.

3. Taking profits: If one wishes to take profit in the investment property, unlike a stock one cannot sell off a few shares and thus control the taxes. The whole property must be sold. While $500K capital gains exclusion for a couple used to be unimaginable outside of CA, it comes fast these days. Yes, first world problem.

4. Step up in basis after death: Given that this is constantly considered for elimination, and we have learned from the changes in how Traditional IRAs are to be inherited that the Gov't is happy to eliminate tax benefits, having to sell the entire property upon inheritance would trigger a huge tax bill for our kids and trigger a huge reduction in investment profitability. Our kids have no desire to own real estate investments.

5. Higher Gov't interference: Risks from increased Gov't regulation became clear with the elimination of the ability to evict for non-payment of rent during Covid. A friend nearly lost her property when her tenants refused to pay, while she of course still needed to pay the mortgage on that property. She still has not recovered financially from that. Now our area is talking about rent controls....

Yes, in the past the small real estate investor could do well, and it made a great diversification from stocks. I always considered real estate the bond portion of our portfolio, however, and did not measure it against the stock market. It slayed bonds. We are down to two properties now, neither of which are rentals, with our primary residence being on the market. Given today's market it looks as though we will continue to have two properties for the foreseeable future, but that's OK, as I have back up options for it. Never be forced to sell.

IP

No. of Recommendations: 2

When there are eight (8) medium sized commercial haul away construction dumpsters of stuff taken out of one (1) house, you get insights into how the Dopamine effects drive folks to repeatedly buy crap stuff. In this clean-up journey we also witnessed the role of landfill space. Siting and approving new landfills is quite difficult. If Waste Management or Republic Services ever have a market swoon to a Buffett type PE, I will be loading up the truck. There are hundreds of thousands homes with crap that someone will one day be hauling to a landfill. Landfill dumping fees continue to rise because of all the above factors.

Interesting. However there have been recent articles on how the tariffs will force the US to become a Yard Sale nation, with people buying used to avoid the higher costs of importing new. IMO it sounds in line with the younger generations. I think of things like the freecycle movement, Facebook Marketplace, etc. Could be those prices decline for a reason.

IP

No. of Recommendations: 2

I think the key is the 'highly desired market".

I live in a former logging town gone resort boom town. In the last 15 years the median price has gone from 200k to 800k, but the riverfront properties have doubled that gain, from 500k to 4 million. I'm surrounded by real estate multi-millionaires. When I point out that BRK has gone from 100k to 800k in the same time, they correctly point out that their investment also gave them a place to live and RE is the easiest of all investments to apply a bit of debt related leverage. I hope they recognize they were lucky, and that RE is not often that lucrative.

Yup. This is in part what I mean by look for properties with constraints to competition. There's only so much waterfront, some less easily developed than others. And the inefficiencies of the market can be seen with our primary residence that was priced without consideration of it being lakefront. Admittedly, it was not lake view at the time, though we have taken care of that. Our second property is on a river, but much more rural so it's value will no likely decline as work from home starts to ebb, but I am not selling this place. It too had no mention of waterfront in the listing, and not even a picture of the very overgrown river bank which we have since cleared to a very long view, but because we already loved the river for kayaking, and had been vacationing here for 4 years, we knew to check it out. There are good opportunities out there, but it has been more of a labor of love than a pure investment. If we had to include all the manhours spent searching for investable properties, it would be hard to justify as an investment. I do love a bargain hunt though.

IP

No. of Recommendations: 2

Yep, luck plays a big role, like they say in real estate ... location, location, location.

No reason not to be both lucky and good. Applying the proper thought process to choice of location absolutely increases your chance of being lucky, and should at least give you a good investment if not an amazing one.

IP,

who has always said that luck is defined by having the brain to look for the right data and the guts to act on the information

No. of Recommendations: 2

You missed the tax bill by a mile. A house nearby just sold for 4.1 million. Taxes 15 years ago were $4000, and have gone up to $10,000.This is generally only true in states with a property tax increase limit (like prop 13 in CA, or homesteading in FL). In a place like NJ, a $4M home would have property taxes around $75k (

https://smartasset.com/taxes/new-jersey-property-t...). In IL it would be similar or a bit higher. In NY, it might a bit lower at $65k. In TX it would also be about $65k, but it depends where exactly in TX.

But that is truly incredible! Where in the USA are taxes on a $4M property only $10k??? Wow!

No. of Recommendations: 2

But that is truly incredible! Where in the USA are taxes on a $4M property only $10k??? Wow!

Maybe not that rare. We own a second house in a sporty and artsy town in New Mexico (I know, bad investment but we like it). Tax rates are very similar. We did have a house in New Hampshire in a town with very few second homes, and taxes were astronomical.

No. of Recommendations: 8

In TX it would also be about $65k, but it depends where exactly in TX. But that is truly incredible! Where in the USA are taxes on a $4M property only $10k??? Wow!

In central London UK (City of Westminster), property taxes for both levels of local government for a �4 million house are �2,034.36 per year. Or, for any property more valuable too. Strange. Apparently it's because Westminster has an unusually broad set of revenues, like parking.

Of course what the tax man giveth, the tax man taketh away. The land transfer taxes (stamp duty) are pretty brutal. Extras for second residences, extras for non residents, maybe 17% of purchase price depending on the price of the place.

Jim

No. of Recommendations: 0

<<Where in the USA are taxes on a $4M property only $10k???>>

We own a second house in a sporty and artsy town in New Mexico (I know, bad investment but we like it). Tax rates are very similar.This site says New Mexico property tax would be about $31k on a $4M house. That's low, but not $10k low.

https://smartasset.com/taxes/new-mexico-property-t...

No. of Recommendations: 1

Our New Mexico home is more modest but the tax rate is far lower than that, about 3.2k on a million dollar house. The area is well endowed with upscale second homes and ski houses so the revenue is high. The practice of funding schools from local property taxes results in an interesting regressive tax structure.

No. of Recommendations: 2

This is generally only true in states with a property tax increase limit (like prop 13 in CA, or homesteading in FL).

In CA, with prop 13, the property tax on a recently sold $4.1M house is about $50K/year.

Elan

No. of Recommendations: 1

In CA, with prop 13, the property tax on a recently sold $4.1M house is about $50K/year.

Yes! But the house in question was purchased 15 years ago for $500k. Since CA only allows tax assessment to go up by 2% a year, it would still have a very low tax payment. That's why I mentioned prop 13.

{kind=link}