No. of Recommendations: 23

It�s an oversized position for me, flattish sales growth & it�s up $20 in 3 weeks, it felt reasonable.This seems sound. Indeed half of the

past increase the quote of Apple since 2014 has been the increase in the valuation multiple, rather than the increase in those past sales itself. Sales per share rose 3.4x over the last decade (2014 - 2024), but the price to sales valuation multiple rose 3.1x over the same period. If Apple was not discounted so much in 2014 the viewers of the quote would consider Apple as a rather �mediocre stock� or even stagnating, but people react to quotes and when looking back Apple still appears like dynamite right now. The share price has risen about 10x over the decade!

Keep in mind that the growth of the underlying business was not 3.4x, as much of that sales per share growth was from the reduction in shares outstanding. Apple do not have a culture of making large acquisitions *thank goodness* and Apple's shares outstanding have fallen 42% over the last decade. This is good, and a symptom of having such small capital expenditure and research requirements in comparison to the colossal cash they are generating, and at least some capital allocation discipline - though keep in mind, they would have done similarly by just being an index fund and holding the portfolio. It is much more trendy to buy your own stock than an index fund these days.

As an investment from today for the next decade, anything can change with valuation multiples but if remaining around 28x earnings I think the investment will be at least adequate.

As for Apple the company, ignoring valuation for a moment: The moat is intact, and an unusually strong one. I prepared some articles (a 6 part series) for TMF on Apple as the perfect investment (the articles published February 2012), not because I projected incredible growth but because the valuation multiple was extremely low relative to the dependability of the future and earnings. But regarding the moat, a lot of it comes from the OS/hardware coupling with the real value in the software, not the hardware. The hardware makes the coupling work, but much of the real moat is the profound momentum from developers having their livelihood depending on their commitment to Apple's ecosystem. When people learn something like they like to continue to use that knowledge. This is largely what caused IBM compatibles to become so dominant in the 1980s - it wasn't the technology, but the self perpetuating momentum between developer community's commitment increasing value of the products, leading to a larger audience in turn bringing more development commitment, and the feedback continuing.

The main investment thesis was obviously success but is now all over as the terrific valuation discount has gone - I don�t think it is particularly high at 28x earnings considering their enormous developer community and other aspects of their moat, however from here you can only reasonably rely on sales growth (not merely the buybacks and dividends) for any real

outperforming investment return. The valuation might remain high, might become lower, but you definitely should not depend on it continuing to rise as it has been the last decade.

So that leaves us with the future sales. They are growing on trend at about 8% per year (though sales per share growing faster than that owing to the consistent buybacks). Let's say about 4% above inflation. Looking into the future, note that Apple�s main sales will very likely, by their nature, remain overwhelmingly with the consumer. This is one problem than dampens my enthusiasm more than anything else: There is only so much you can extract from people�s pockets each year.. so there is an economic limit once you have market dominance.*

The Vision Pro was a once-in-a-decade product (regarding planning and delivery), and take up is lower than I expected. Around half of that I speculate is the sheer unfamiliarity (which will partly be overcome with time) - it takes years for the public to get used to such an odd thing even if it is actually useful. The second half of the problem is that the software is in such early days and there are almost no apps (which will definitely be overcome with time), so

there is a lot of life ahead regarding the value of the device. But my earlier view of perhaps 50 million units by 2028 might be more like 20 million or so, even if it follows the usual S curve with the main growth three or four years from now.

I have always firmly held the view that Apple can retain the iPhone as a premium product with strong margins (thus a high price). People value their iPhone considerably more than they pay. I was stunned by this idea a decade ago - Apple wanted mass adoption but if they doubled their price I expect they would have still sold an amazing number despite being priced far above the competition. The mass adoption is critical for their economic moat with its development community, but they

do have more pricing power than I believe most people understand - and the magic isn't in the hardware but in the software; all our attention, and what we are drawn in by, is the software.

But the problem with consumer products once you have market dominance, is that you start to hit limits with many people paying to Apple a huge percent of their available disposable income. You cannot raise the per capita cash extraction level continuously, and they are hitting limits with the capita part also.

A company like Google is quite different in this way as it

still have a long runway ahead for online advertising spending. Advertising expenditure will be a lot higher in ten years than it is today. Even non-profit entities need to use advertising (sometimes the bulk of their expense) to get their message out.

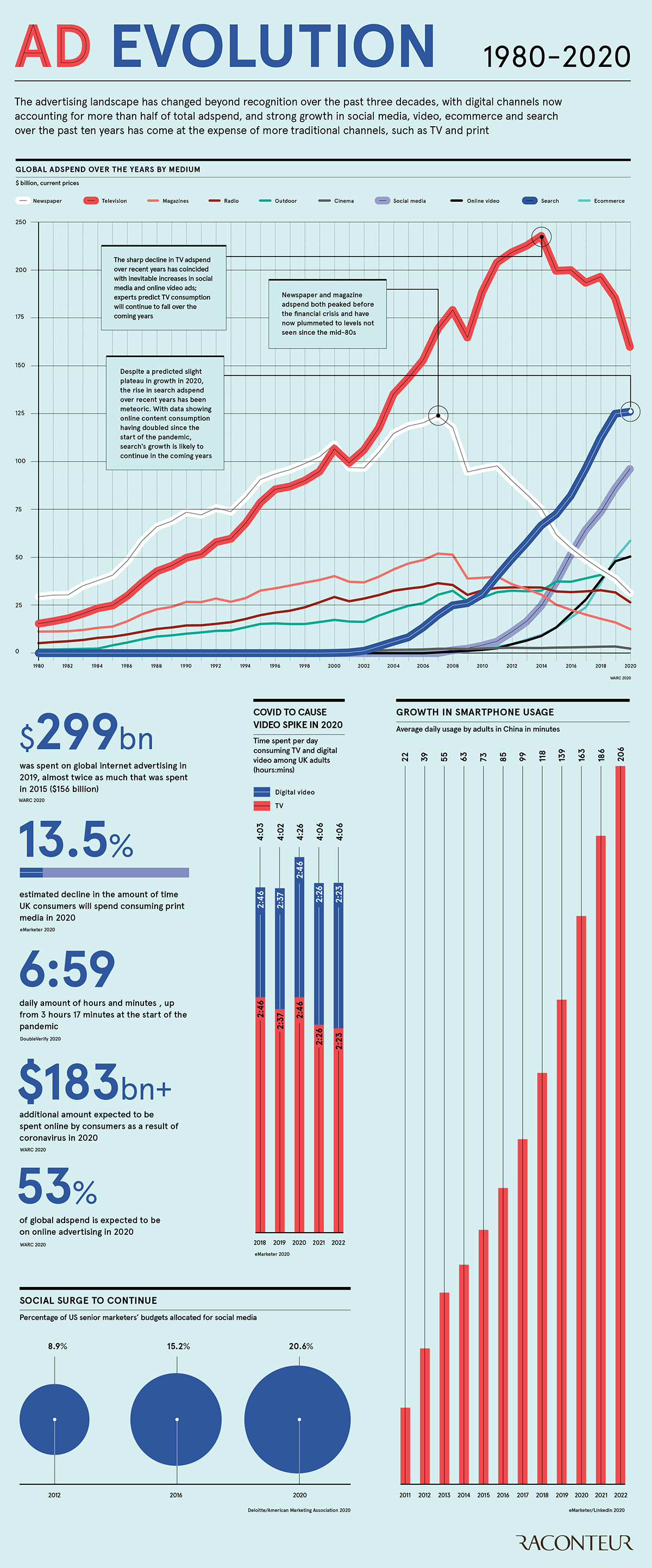

The following chart which shows how online advertising is still mid process in eating up the other forms of marketing - why do I think this growth will continue for a long time? Because present online marketing is very very inefficient (think about how many adverts you ignore), so return on expenditure is ridiculously lower than it will be 10 or 20 years from now when the targeting is much more effective, so the amount that businesses will be willing to pay for advertising (as targeting efficiency increase) I predict will increase more than most imagine:

https://www.visualcapitalist.com/wp-content/upload...Returning to Apple, they likely do have an opportunity to grow their services far more than presently. I like to ask myself how much I am spending on hardware every few years, and next ask how much I spend on services to Apple. Can you imagine the amount that you pay for the phone/laptop doubling? Can you imagine your services expenditure doubling? I expect may will say yes to the second question and not the first. This will result in the services line of business still having quite some room to expand, despite the market saturation at the product level.

Apple�s sales growth (and roughly equivalent earnings growth their huge stable margins) might be similar or worse than they have been, and gains from higher valuation from here can�t be relied on. I'll compare the past with a conceivable future.

Last 10 years:

-------------

Sales increased ~2.1x.

Sales per share grew ~3.4x.

Valuation multiple increased 3.1x.

Next 10 years

-------------

Sales increased 1.8x (moat well preserved, pricing power and services increase, Vision Pro stars contributing 4 years from now as auxiliary product to iPhone and not replacing, the already dwindled 15% of sales in China continues to not provide any growth)

Sales per share grows ~3x with 40% more shares purchased (1.8 / 0.6 = 3).

Margins retained.

Valuation multiple decreases 0.7x (to get from a PE of 28 to 20).

For IV10 you need to add the dividends back as part of the accumulated value, and I usually give a small return for them, so I just add them up and multiple by 1.6. So 10 years of 0.5% yielding dividends gives, times 1.6, gives another 8% of value.

Combining the above, we have IV10/price

= EPS growth * change in valuation multiple * value gain from dividend = 3 * 0.7 * 1.08

= ~2.3.

In other words you will probably more than double your money by investing in Apple now, presuming you are able to exit reliably at a PE of 20. The historical average market EPS multiple is 15.

The 2014 days of Apple's IV10/price ratio near 5.0 are over, but an IV10/price of 2.3 is pretty respectable and somewhere on par with the market average.

In any case, having a similar return to an equal weighted index, with *one large* investment, requires the investment to not only have an average return but also be very safe - which is very hard to find in combination. Because of that, Berkshire Hathaway holding Apple is more sound than it first looks. I would personally sell the whole lot today and replace it with Google or Brookfield Corporation, but that's just me.

- Manlobbi

{kind=link}